by Deepak Madan | May 13, 2026 | Blog

IEC Registration in India: The Key to Successful International Trade

IEC Registration in India is mandatory for businesses involved in import and export activities. Issued by the Directorate General of Foreign Trade, the Import Export Code enables businesses to conduct international trade legally, clear customs shipments, and receive international payments smoothly.

What is an IEC?

An IEC (Import Export Code) is a 10-digit business identification number issued by the Directorate General of Foreign Trade that is mandatory for importing or exporting goods and services from India.

Businesses need an IEC to:

- Clear shipments through customs

- Receive international payments

- Conduct legal international trade

- Expand business globally

Without an IEC, businesses cannot legally participate in import-export activities in India.

Why is IEC Important for Importers and Exporters?

The Import Export Code acts as the foundation of international trade operations. Whether a business imports products, exports goods, or provides services internationally, IEC is essential for compliance and smooth transactions.

Benefits of IEC for Businesses

1. Enables International Trade

IEC allows businesses to import and export products legally from India.

2. Required for Customs Clearance

Indian customs authorities require IEC during shipment processing.

3. Helps Receive International Payments

Exporters need IEC to receive foreign currency payments through banks.

4. Expands Global Business Opportunities

Businesses with IEC can access international markets and customers.

5. No Renewal Requirement

In most cases, IEC remains valid for a lifetime unless surrendered or canceled.

Who Needs an IEC in India?

IEC is required for:

- Importers

- Exporters

- E-commerce exporters

- Manufacturers

- Service providers dealing internationally

- Amazon and online marketplace exporters

- Freelancers receiving international business payments (in some cases)

Is IEC Mandatory for Export and Import?

Yes. IEC is mandatory for most import-export activities in India.

Without IEC:

- Businesses cannot clear shipments

- Banks may not process export-import transactions

- International trade operations become restricted

However, certain government departments and notified exemptions may not require IEC.

Who Issues the IEC in India?

The Import Export Code is issued by the Directorate General of Foreign Trade under the Ministry of Commerce and Industry, Government of India.

The IEC application process is completed online through the DGFT portal.

Documents Required for IEC Registration in India

Businesses generally require the following documents for IEC application:

| Document |

Required |

| PAN Card |

Yes |

| Aadhaar Card |

Yes |

| Business Address Proof |

Yes |

| Bank Account Details |

Yes |

| Cancelled Cheque / Bank Certificate |

Yes |

| Mobile Number & Email ID |

Yes |

How to Apply for IEC Registration in India

The process of IEC Registration in India is completed online through the DGFT portal.

Step 1: Visit the DGFT Portal

Access the official DGFT website and create an account.

Step 2: Fill the IEC Application Form

Enter business details such as:

- PAN details

- Business type

- Address

- Bank information

Step 3: Upload Required Documents

Upload all necessary documents for verification.

Step 4: Pay the Application Fee

Complete the online payment process.

Step 5: Receive IEC Certificate

After successful verification, the IEC certificate is issued digitally.

How Long Does IEC Approval Take?

IEC approval is generally processed within 1–7 working days if all documents and details are correct.

Processing time may vary depending on:

- Verification requirements

- Document accuracy

- Application completeness

Common IEC Application Mistakes Businesses Make

Many applications get delayed due to avoidable errors.

Common Mistakes Include:

- Incorrect PAN details

- Wrong bank account information

- Mismatch in address proof

- Incomplete documentation

- Incorrect business category selection

Carefully reviewing the application before submission helps avoid delays.

Why IEC is Important for E-Commerce Exporters

Businesses selling products internationally through platforms like Amazon or other marketplaces often require IEC for export transactions.

IEC helps:

- Receive export payments

- Complete customs formalities

- Ship products internationally

This makes IEC essential for businesses planning to scale globally.

Can Individuals Apply for IEC?

Yes. Individuals involved in international business activities, freelancing, consulting, or exports may apply for IEC depending on the nature of transactions.

Do Service Exporters Need IEC?

Service exporters receiving payments in foreign currency may also require IEC in certain cases, especially when dealing with international clients and banks.

Is IEC Renewal Required?

IEC generally does not require frequent renewal. However, businesses may need to update or confirm IEC details periodically as per DGFT regulations.

What Happens Without IEC?

Without an IEC:

- Import-export shipments may be blocked

- International payments may face issues

- Customs clearance may not be possible

- Businesses cannot legally trade internationally

IEC is therefore a critical requirement for global business operations.

FAQs About IEC

What is the full form of IEC?

IEC stands for Import Export Code.

Is IEC Registration in India mandatory for exporters?

Yes, IEC is mandatory for most export activities in India.

Who issues IEC?

IEC is issued by the Directorate General of Foreign Trade.

Can a freelancer apply for IEC?

Yes, freelancers involved in international transactions may apply depending on business requirements.

Is IEC valid for lifetime?

In most cases, IEC remains valid for lifetime unless canceled or surrendered.

Can I export on Amazon without IEC?

Most international e-commerce export activities require IEC.

How much time does IEC registration take?

IEC approval generally takes between 1–7 working days.

What documents are required for IEC?

PAN card, Aadhaar card, address proof, and bank details are commonly required.

Final Thoughts

IEC Registration in India is one of the most important requirements for businesses planning to expand into global trade. Whether you are an importer, exporter, startup, manufacturer, or online seller, obtaining an IEC is the first step toward successful global trade.

With growing international business opportunities, having the right compliance framework helps businesses expand confidently and operate smoothly across borders.

by Deepak Madan | Apr 25, 2026 | Exchange Rate API

RBI Reference Rate API – A Must-Have Tool for Exporters, Importers & Fintech Platforms

If your business deals in foreign currency, one number impacts your financial accuracy every day:

👉 The RBI Reference Rate

From accounting to audits, this rate is the standard benchmark across India.

But accessing and managing it manually? That’s where problems begin.

What is the RBI Reference Rate?

The Reserve Bank of India publishes daily reference exchange rates for major currencies such as USD, EUR, GBP, and JPY against the INR.

These rates are:

- Published every working day

- Based on interbank market averages

- Used as an official benchmark rate in India

Why RBI Reference Rates Matter for Exporters & Importers

-

Accounting & Book Closing

Exporters and importers use RBI reference rates to:

- Convert foreign currency receivables/payables

- Record transactions in books

- Prepare financial statements

👉 Example:

An exporter receiving USD payments will convert USD to INR using the RBI reference rate for accounting.

-

Forex Gain/Loss Calculation

Businesses regularly calculate the following:

- Unrealized forex gain/loss

- MTM (Mark-to-Market) adjustments

👉 RBI rate becomes the standard benchmark for valuation.

-

Compliance & Audits

Auditors and regulators prefer:

- RBI reference rate as official benchmark

- Consistent valuation across financial periods

-

Internal MIS & Reporting

Companies use RBI rates for:

- Daily MIS reporting

- Treasury dashboards

- Exposure tracking

The Problem with RBI Rate Access

❌ No official RBI API

❌ Manual website tracking

❌ Time-consuming process

❌ Risk of inconsistent data

Solution: RBI Reference Rate API by IBRLIVE

IBRLIVE offers a reliable and automated RBI Reference Rate API for businesses that need accuracy and speed.

Key Features

- ✅ Daily RBI rates (automated)

- ✅ Historical data access

- ✅ Easy API integration

- ✅ Clean JSON format

Sample API Response

Who Should Use This API?

- Exporters & Importers

- CA Firms & Auditors

- ERP platforms (SAP, Tally)

- Fintech & Forex companies

Benefits of RBI Reference Rate API

Save Time

No manual tracking required

Improve Accuracy

Use official benchmark rates

Reduce Audit Risk

Consistent data across reports

Better Financial Control

Make informed decisions

Why Businesses Are Switching to APIs

Manual tracking:

- Slows down operations

- Increases risk

Automation:

- Improves efficiency

- Ensures compliance

Why Choose IBRLIVE API?

- Fast & reliable

- Accurate official data

- Easy integration

- Cost-effective

How to Get Started

- Request API access

- Integrate with ERP/accounting system

- Automate daily forex updates

FAQs

What is the RBI reference rate used for?

It is used for accounting, reporting, and forex valuation.

Is the RBI API available?

No, RBI does not provide a public API.

How often is the RBI rate updated?

It is updated every working day.

Final Thought

RBI reference rates are the foundation of financial accuracy.

If your data is wrong, your decisions will be too.

Start Using RBI Reference Rate API with IBRLIVE

Accurate. Automated. Reliable.

by Deepak Madan | Apr 25, 2026 | Exchange Rate API

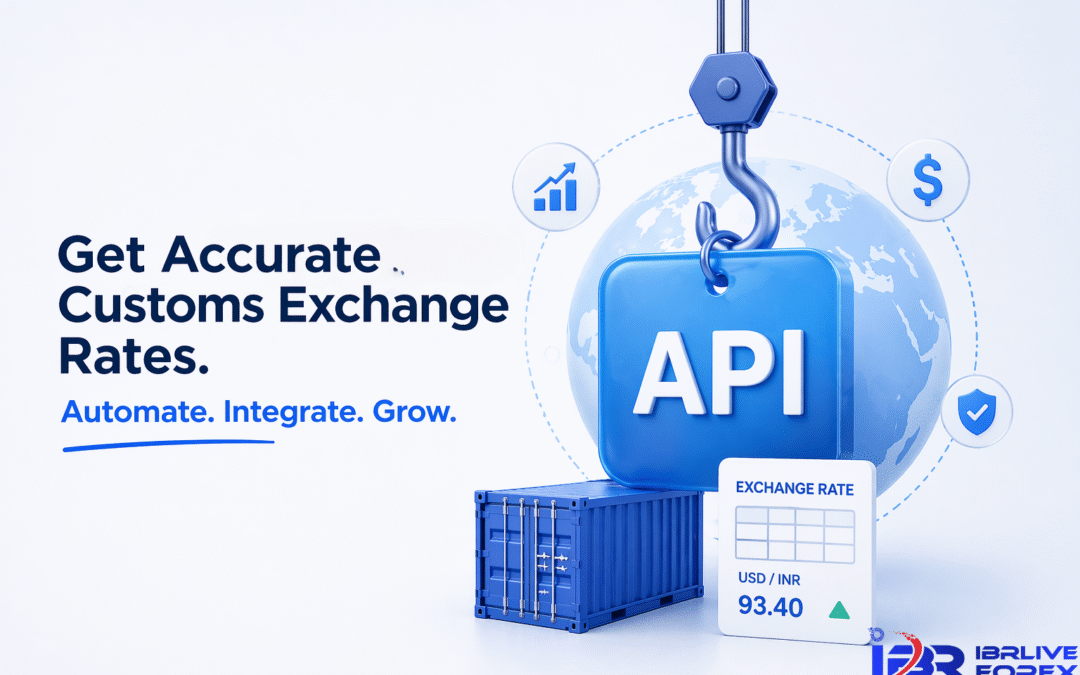

Customs Exchange Rate API for ICEGATE Rates in India

If you’re an importer or exporter, your profit margins depend on one critical factor:

👉 The customs exchange rate used in import duty calculation

Yet most businesses still rely on manual tracking from ICEGATE, leading to delays, errors, and incorrect costing.

This is exactly where a Customs Exchange Rate API gives you a competitive edge.

What is the Customs Exchange Rate (ICEGATE)?

Customs exchange rates are published on the ICEGATE portal and used for:

- Import duty calculation

- Export valuation

These rates are:

- Issued periodically (usually fortnightly)

- Based on SBI rates

- Legally applicable for customs clearance

👉 Even a ₹0.50 difference can impact your total landed cost significantly.

Why Customs Rates Are Critical for Businesses

- Import Duty Calculation

Importers must use customs rates to calculate the following:

- Assessable value

- Basic customs duty

- IGST

👉 Even small rate differences can impact landed cost significantly.

- Export Documentation

Exporters use customs rates for:

- Shipping bills

- Invoice valuation

- Compliance filings

- Pricing & Costing Decisions

Importers rely on these rates for the following:

- Product costing

- Margin calculations

- Purchase decisions

- Avoiding Compliance Issues

Using incorrect exchange rates can lead to:

- Penalties

- Delays in clearance

- Disputes with customs

How the Customs Exchange Rate Impacts Import Duty

When calculating import duty, the exchange rate is used to convert:

👉 CIF value (Cost + Insurance + Freight) → INR

This directly affects:

- Basic Customs Duty (BCD)

- IGST

- Total import cost

Example:

- CIF Value: $10,000

- Customs Rate: ₹93.40

👉 Converted Value = ₹934,000

Now apply duties → your final cost changes based on this rate.

The Problem with ICEGATE Exchange Rate Access

Businesses today face the following:

❌ No official API from ICEGATE

❌ Manual tracking from website

❌ Delays in updates

❌ High risk of human error

👉 This becomes a serious issue when scaling operations.

Solution: Customs Exchange Rate API by IBRLIVE

IBRLIVE provides a fully automated Customs Exchange Rate API that eliminates manual effort and ensures accuracy.

Key Features

- ✅ Latest import & export exchange rates

- ✅ Historical ICEGATE data

- ✅ Real-time updates

- ✅ Easy ERP integration

- ✅ Clean JSON API format

Sample API Response

Who Should Use This API?

- Importers & Exporters

- Custom House Agents (CHA)

- Logistics companies

- ERP / Accounting platforms

Benefits of Using the Customs Exchange Rate API

⏱ Save Time

No more manual ICEGATE tracking

📉 Reduce Costing Errors

Accurate forex conversion

📦 Faster Processing

Avoid delays in customs clearance

📊 Better Decision Making

Real-time data = better margins

Why Automation is No Longer Optional

If you are:

- Handling multiple imports

- Managing ERP systems

- Scaling operations

👉 Manual processes will slow you down.

Automation is not a luxury—it’s a necessity.

How to Get Started

- Request API access from IBRLIVE

- Integrate with your system

- Start receiving automated customs exchange rates

FAQs

Which exchange rate is used for import duty in India?

Customs notified exchange rate (ICEGATE) is used.

Can I use a live forex rate?

No, only customs rates are valid for duty calculation.

Is there an official ICEGATE API?

No, currently there is no public API available.

Final Thought

Customs exchange rates directly impact your cost, compliance, and competitiveness.

If you’re still relying on manual processes, you’re leaving money—and efficiency—on the table.

👉 Start Automating Customs Exchange Rates with IBRLIVE

Accurate. Automated. Scalable.

by Deepak Madan | Sep 6, 2025 | Scrip Transfer

“ICEGATE scrip transfer is the official and compliant way to ROSCTL and RODTEP License Sale and buying and applying scrips for customs duty payment in India.”

Trading in RODTEP and ROSCTL scrips can unlock great value for both exporters and importers — but only if you follow the correct procedures. Whether you are selling your e-scrips on the ICEGATE portal or buying them for customs duty payment, keeping the following points in mind will help you secure better rates, avoid delays, and stay compliant with DGFT and CBIC guidelines.

✅ Consolidate Scrips Port-Wise for Higher Value

If your ICEGATE Scrip Ledger shows multiple scrips across different ports—say 5 for INNSA1 and 5 for INBOM4—consolidate port-wise. Generate a single RODTEP or ROSCTL scrip per port. Why? Large-value scrips attract better rates in the market, and buyers prefer fewer, higher-value e-scrips to save on paperwork and ICEGATE transaction time. You single large value RODTEP License Sale will attract better rates.

✅ Always Deal with Verified Buyers & Sellers

Whether you’re buying scrips to save on customs duty or selling them to monetize export incentives, ensure your counterparty is KYC-verified. Dealing with unverified parties increases the risk of fraud, delayed payments, and non-compliant transfers — something no exporter or importer should take lightly. Use platforms like IBRLIVE.com that work only with vetted traders.

✅ Wait & Consolidate for Better Scrip Rates

Don’t rush to sell small-value RODTEP scrips. Instead, wait for more scrips to get generated in your account and then consolidate them port-wise. This not only reduces the number of transactions but also helps fetch higher RODTEP scrip rates due to increased demand for larger scrips.

✅ Check ICEGATE Scrip Ledger to Avoid Expired Incentives

Many exporters miss out on their RODTEP and ROSCTL scrips simply because they never check their ICEGATE scrip ledger. These e-scrips are often automatically credited based on your shipping bill scrolls, but if you don’t act on them in time, they may expire unused. Also, several exporters are unaware that their product category is eligible for RODTEP/ROSCTL benefits. Always log in to your ICEGATE account and review your e-scrip ledger periodically to avoid losing valuable export incentives.

✅ Send Required Original Documents Without Delay

Importers need the original documents — Invoice, Transfer Letter (countersigned by bank), and Declaration — to complete their customs duty payment via scrips. Delay in submitting these documents could result in cancellation of the deal or loss of trust. Ensure all documents are dispatched immediately post-transfer.

✅ Take Screenshot of Port Code During Scrip Generation

Always take a screenshot of the generated e-scrip that clearly displays the port code. This is a mandatory practice. If missed, importers may ask for one shipping bill copy per scrip to confirm the port, delaying your transaction and reducing buyer interest.

✅ Use Mobile OTP on ICEGATE Instead of Email OTP

ICEGATE now supports mobile OTP for scrip transfers and receipts. It is faster and more reliable than email-based OTPs. Always register your updated mobile number with ICEGATE and prefer mobile OTP for timely transaction execution.

✅ Avoid Multiple OTP Resend Attempts — ICEGATE May Block You

Never hit resend OTP more than 3 times on ICEGATE. This may block your ID temporarily, stalling your scrip transfer. Instead, log out and retry after a few minutes for a smooth experience.

✅ Don’t Panic if Exporter Delays Transfer After Payment

If you’re an importer and have made the payment but the exporter hasn’t transferred the scrips, stay calm. You can escalate the issue to ICEGATE customer care. For secure trading, use a trusted platform like IBRLIVE, which ensures timely transfer upon payment.

✅ Exporter Transferred Scrips But No Payment Received? Call ICEGATE

In cases where the exporter has Sell RODTEP or Sell ROSCTL and transferred the scrip but the importer fails to make the payment, you can approach ICEGATE or seek assistance from trading platforms like IBRLIVE. Escrow-secured platforms reduce this risk considerably.

RODTEP scheme and ROSCTL scheme scrips are powerful tools for cost saving and liquidity management — but only if handled with care. Exporters and importers must follow best practices to avoid delays, ensure compliance with DGFT and CBIC regulations, and maximize returns.

To trade securely and instantly, visit 👉 https://ibrlive.com/buy-sell-rodtep-rosctl

Related Blogs You Might Like:

by Deepak Madan | May 8, 2025 | Scrip Transfer

The RoDTEP export incentive scheme India, or Remission of Duties and Taxes on Exported Products, is one of the most significant initiatives introduced by the Government of India to support exporters and boost international trade competitiveness. Launched in September 2019, this RoDTEP new export scheme was designed to refund taxes and duties that were previously not reimbursed under earlier programs, providing exporters with a fair and transparent refund mechanism. RODTEP Benefits are explained in the blog in detail.

What is the RoDTEP Scheme and Why Was It Introduced?

Before the RoDTEP scheme came into effect, exporters benefited from earlier incentive programs such as the Merchandise Exports from India Scheme (MEIS) and the Rebate of State Levies (ROSL). However, these schemes were found to be non-compliant with World Trade Organization (WTO) guidelines. To ensure full compliance and continued export competitiveness, the MEIS scheme was replaced by RoDTEP on January 1, 2021.

The Ministry of Commerce and Industry, along with the Directorate General of Foreign Trade (DGFT), implemented the RoDTEP DGFT system to streamline the refund process through electronic scrip issuance and seamless credit transfer.

How Does the RoDTEP Export Incentive Scheme Work?

Under the RoDTEP export incentive scheme India, exporters can claim refunds for various taxes and duties that were earlier embedded in the cost of exported goods but not refunded through any other scheme. These include:

-

Central and state excise duties on fuel used for transport and production

-

VAT and central sales tax on raw materials

-

Electricity duties

-

Mandi tax, stamp duty, and other local levies

These refunds are issued as RoDTEP scrips, which can be utilized for payment of customs duties or sold in the open market for cash.

The refund rate varies depending on the product category and sector. Rates are determined by the Department of Commerce with inputs from industry bodies and other government departments to ensure that they remain financially sustainable while supporting exporter profitability.

Key Benefits of the RoDTEP Scheme for Exporters

The RoDTEP benefits extend across multiple industries, making it one of the most impactful export policies in recent years. Some of the major advantages include:

- Enhanced global competitiveness through cost reduction on exported goods.

-

Compliance with WTO norms, ensuring the continuity of export incentives.

-

Automated and transparent refund process through the DGFT portal.

-

Eligibility for a wide range of sectors, including textiles, leather, agriculture, handicrafts, marine products, and more.

-

Ease of scrip trading, allowing exporters to monetize their incentives quickly.

For many exporters, especially MSMEs, this scheme provides much-needed financial relief amid challenges like volatile currency movements, high input costs, and intense international competition.

Step-by-Step Process to Sell RoDTEP Scrips

Exporters who receive RoDTEP scrips can either use them to pay customs duties or sell them for cash in the open market. Below is a simplified guide to help you sell your scrips efficiently:

-

Eligibility Check:

You must be an exporter who has been issued RoDTEP scrips by the DGFT.

-

DGFT Registration:

Ensure you are registered with the Directorate General of Foreign Trade (DGFT) and possess a valid Import Export Code (IEC).

-

Find a Recognized Buyer:

Only recognized agencies or platforms can purchase these scrips. It’s important to choose a reliable partner for smooth transactions.

-

Submit Required Documents:

Provide necessary paperwork, including invoices, shipping bills, and export declarations, along with your RoDTEP scrips.

-

Negotiate Pricing:

The market price of RoDTEP scrips depends on supply, demand, and product category. You can contact the expert team at IBRLIVE.com to get competitive rates and quick settlements.

-

Receive Payment:

Once the price is agreed upon, the payment is processed, allowing you to reinvest funds back into your business.

Why Choose IBRLIVE for Selling RoDTEP Scrips

At IBRLIVE, we simplify the process of buying and selling RoDTEP scrips with complete transparency and trust. Our team ensures that exporters receive the best market rates and hassle-free documentation support. Whether you’re a first-time exporter or a large-scale manufacturer, we help you unlock the full potential of your RoDTEP export incentive scheme India benefits efficiently.

Conclusion

The RoDTEP export incentive scheme India represents a crucial step toward strengthening India’s position in global trade. By refunding unrebated taxes and duties, the government has empowered exporters to compete globally while maintaining compliance with international norms. For exporters looking to monetize their RoDTEP scrips quickly and securely, partnering with trusted experts like IBRLIVE can make the entire process seamless and profitable.

Top 5 FAQs on the RoDTEP Export Incentive Scheme India

1. What is the RoDTEP export incentive scheme India?

The RoDTEP export incentive scheme India (Remission of Duties and Taxes on Exported Products) is a government initiative that refunds previously unclaimed taxes and duties to exporters. It helps make Indian goods more competitive in global markets by reducing hidden export costs.

2. What is the difference between MEIS and RoDTEP?

The MEIS scheme was replaced by RoDTEP in January 2021 to ensure compliance with WTO norms. Unlike MEIS, which offered fixed export incentives, RoDTEP provides tax refunds based on actual duties and levies paid on exported goods, making it more transparent and WTO-compliant.

3. How can exporters claim RoDTEP benefits through DGFT?

Exporters can claim RoDTEP DGFT refunds by logging into the DGFT portal, filing export shipping bills, and selecting RoDTEP under the reward scheme option. Once approved, the DGFT credits RoDTEP scrips to the exporter’s electronic ledger, which can be used or sold for cash.

4. Can RoDTEP scrips be sold or transferred?

Yes, exporters can sell or transfer RoDTEP scrips in the open market. The process involves finding a recognized buyer or agency, submitting required export documents, and negotiating a fair price. You can contact IBRLIVE to sell RoDTEP scrips quickly at competitive market rates.

5. Which industries benefit most from the RoDTEP scheme?

The RoDTEP new export scheme benefits several sectors, including textiles, leather, agriculture, marine products, and handicrafts. These industries gain from reduced export costs, better refund visibility, and improved global competitiveness.

Related Blogs You Might Like: