Tax Collected at Source (TCS) on foreign remittances has become an important consideration for individuals sending money abroad under the Liberalised Remittance Scheme (LRS). Whether you are paying tuition fees, investing in foreign stocks, booking overseas tour packages, or supporting family members abroad, understanding the details of tax collected at source helps you plan your finances better.

In Budget 2025, the government increased the TCS threshold on foreign remittances from ₹7 lakh to ₹10 lakh, providing relief to many resident Indians making smaller overseas payments.

This guide explains:

What is Tax Collected at Source?

Latest TCS slab rates for FY 2025-26

TCS on education, travel, investments, and medical remittances

How to claim TCS refund

Exemptions and important rules under LRS

What is TCS? –

What is Tax Collected at Source (TCS)? Tax Collected at Source (TCS) is a tax that is collected by authorized dealers or banks when a resident individual sends money abroad under the Liberalized Remittance Scheme (LRS). The amount collected is deposited with the Income Tax Department and reflected in the taxpayer’s Form 26AS. TCS is not an additional tax, it can be adjusted while filing Income Tax Return (ITR).

Tax Collected at Source (TCS) is a tax collected by the authorized dealers or banks when a resident individual remits money abroad under the Liberalised Remittance Scheme (LRS).

The amount collected is deposited with the Income Tax Department and will be reflected in the taxpayer’s Form 26AS. TCS is not an extra tax, it can be adjusted during filing of Income Tax Return (ITR).

Is TCS applicable on foreign remittances?

Yes, as per Section 206C(1G) of the Income Tax Act, Tax Collected at Source (TCS) is applicable on foreign remittances made under the Liberalised Remittance Scheme (LRS) of the Reserve Bank of India (RBI).

From FY 2025-26, TCS is generally applicable only when the total remittance amount exceeds ₹10 lakh in a financial year. The applicable TCS rate depends on the purpose of remittance, such as education, medical treatment, overseas tour packages, foreign investments, or other overseas transfers.

In cases where PAN is not furnished, higher TCS rates may apply as per Income Tax provisions.

The revised ₹10 lakh threshold became effective from April 1, 2025, following Budget 2025 updates.

Are different overseas transactions eligible for TCS?

Yes, various overseas remittances under the Liberalised Remittance Scheme (LRS) are eligible for TCS depending on the nature and amount of the transaction.

These include:

Overseas education payments

Foreign investments in stocks, mutual funds, or property

International tour packages

Medical treatment abroad

Gifts and maintenance sent to relatives overseas

Other permitted current and capital account transactions under LRS

For most remittances, TCS applies only when the total remittance exceeds ₹10 lakh in a financial year. However, overseas tour packages may attract TCS from the first rupee depending on the applicable slab rates.

The following section explains the detailed TCS slab rates for different foreign remittances

Current Account Remittances:

Money sent for overseas education

Money sent for Gifts & Donations

Money sent for medical treatment abroad

Money sent for family maintenance

Money loaded & reloaded in travel card (Forex Card)

Capital Account Remittances:

Loan to relatives

Investment in overseas shares & mutual funds

Investment in properties abroad

For remittances made for education purposes through an education loan obtained from a financial institution under Section 80E, no TCS is applicable from FY 2025-26.

For example, if a student remits ₹12 lakh abroad using an eligible education loan from a bank or recognised financial institution, NIL TCS will be applicable on the entire amount.

However, for self-funded education remittances, TCS becomes applicable only when the total remittance exceeds ₹10 lakh in a financial year. In such cases, a TCS of 5% is charged only on the amount exceeding ₹10 lakh.

For example, if an individual sends ₹15 lakh abroad for education through self-funding:

Up to ₹10 lakh → No TCS

Remaining ₹5 lakh → 5% TCS

Total TCS applicable = ₹25,000

Please also note that the ₹10 lakh threshold is calculated cumulatively for the entire financial year under the Liberalised Remittance Scheme (LRS).

For example, if a person sends:

CAD 10,000 (₹6 lakh equivalent) on 05.04.2025, and

CAD 10,000 (₹6 lakh equivalent) again on 10.10.2025,

Then the total remittance during the financial year becomes ₹12 lakh.

In this case:

First ₹10 lakh → No TCS

Remaining ₹2 lakh → 5% TCS

Total TCS applicable = ₹10,000

The revised threshold and updated TCS provisions were introduced under Budget 2025 effective from April 1, 2025. You can refer to the official Union Budget Tax Reform Document for updated provisions.

Is TCS applicable for import & export of goods and services?

No, TCS under Section 206C(1G) is not applicable on import and export transactions related to goods and services.

The provisions of TCS discussed here apply specifically to foreign remittances made by resident individuals under the Liberalised Remittance Scheme (LRS).

TCS is also generally not applicable on overseas direct investments made by Indian companies, LLPs, partnership firms, or joint ventures outside India under permitted RBI regulations.

Is TCS applicable on overseas tour packages?

Yes, TCS is applicable on overseas tour packages purchased under the Liberalised Remittance Scheme (LRS).

From FY 2025-26:

5% TCS is applicable on overseas tour packages up to ₹10 lakh

20% TCS is applicable on the amount exceeding ₹10 lakh

Unlike many other foreign remittances, TCS on overseas tour packages may apply from the first rupee depending on the applicable slab.

For example:

Tour package value = ₹8 lakh

Applicable TCS = 5%

If the package value exceeds ₹10 lakh, a higher TCS rate may apply on the excess amount.

Can I claim a refund for TCS?

Yes, the TCS amount collected on foreign remittance is reflected in the buyer’s Form 26AS after the authorised dealer or seller files the TCS return.

TCS is not an additional tax. The amount can be adjusted against the taxpayer’s final income tax liability while filing the Income Tax Return (ITR).

If the taxpayer has no tax liability or excess TCS has been collected, the refund can be claimed while filing the ITR.

Latest TCS Changes for FY 2025-26

The Government introduced major updates in TCS provisions on foreign remittances under Budget 2025 effective from April 1, 2025.

Key changes include:

The TCS threshold for foreign remittances under LRS has been increased from ₹7 lakh to ₹10 lakh

Education remittances through loans under Section 80E now attract NIL TCS

Self-funded education and medical remittances above ₹10 lakh attract 5% TCS

Foreign investments, gifts, maintenance transfers, and other LRS remittances above ₹10 lakh attract 20% TCS

Overseas tour packages attract 5% TCS up to ₹10 lakh and 20% on the amount exceeding ₹10 lakh

These changes were introduced to provide relief to students, families, and individuals making smaller overseas remittances.

Let us understand the latest TCS slab rates on foreign remittances for FY 2025-26 with the help of the table below:

Nature of Overseas Transaction

Updated TCS Rate (Effective from 1st April 2025)

Remittance for education through self-funding

NIL up to ₹10 lakh, 5% on amount exceeding ₹10 lakh

Remittance for education through education loan under Section 80E

NIL TCS

Remittance for medical treatment abroad

NIL up to ₹10 lakh, 5% on amount exceeding ₹10 lakh

Remittance for family maintenance, gifts, foreign investments in shares, property & mutual funds

NIL up to ₹10 lakh, 20% on amount exceeding ₹10 lakh

Overseas tour package

5% up to ₹10 lakh, 20% on amount exceeding ₹10 lakh

Other foreign remittances under LRS

NIL up to ₹10 lakh, 20% on amount exceeding ₹10 lakh

FAQs on Tax Collected at Source (TCS)

1. What is tax collected at source and why is it charged?

Tax collected at source is a tax that the seller or service provider collects from the buyer at the time of receiving payment for certain specified transactions. It is charged to ensure early tax compliance and to track high-value transactions under the Income Tax Act.

2. What is the tax collected at source meaning in simple terms?

The tax collected at source meaning refers to a system where tax is collected upfront when a transaction takes place, instead of waiting until the end of the financial year. The collected amount is deposited with the government and later adjusted against the taxpayer’s final tax liability.

3. Where can I find details of Tax Collected at Source deducted on my payments?

The details of Tax Collected at Source (TCS) deducted on foreign remittances can be viewed in your Form 26AS and Annual Information Statement (AIS) available on the Income Tax Department portal.

These statements display:

TCS amount collected

Name of the authorised dealer or collector

Date of tax deposit

Transaction details related to foreign remittance

Taxpayers can use these records while filing their Income Tax Return (ITR) to claim TCS credit or refund, wherever applicable.

4. How does tax collected at source affect an individual’s income tax return?

Tax collected at source is not an extra tax burden. It is treated as a tax credit and can be adjusted while filing your income tax return. If the total tax collected is more than your actual liability, you may claim a refund.

5. Why is understanding tax collected at source meaning important for taxpayers?

Understanding the tax collected at source meaning helps taxpayers plan their cash flow and avoid confusion during tax filing. It also ensures that the collected amount is correctly reflected in tax records and claimed properly.

6. Are details of tax collected at source mandatory to verify before filing returns?

Yes, verifying the details of tax collected at source is important before filing your return to ensure accuracy. Any mismatch between actual collections and reported figures may delay refunds or trigger notices from the tax department.

7. Is tax collected at source applicable to all transactions?

No, tax collected at source applies only to specific transactions notified under the Income Tax Act, such as certain foreign remittances, sale of goods, or high-value transactions, depending on prevailing rules.

8. How is tax collected at source different from other taxes?

The tax collected at source meaning differs from regular income tax because it is collected at the time of transaction rather than calculated at year-end. It acts as a tracking and compliance mechanism rather than a final tax.

NRI Account Rules in India: Banking, Remittances & Taxation Explained

Individuals of Indian origin who live outside India for employment, education, or personal reasons are treated as non-residents under Indian law. A person is classified as non-resident if they stay outside India for more than 182 days in a financial year or leave the country with the intention of settling abroad for an indefinite period.

Understanding NRI account rules is important because financial and banking requirements of overseas Indians differ from resident Indians. To manage these differences, the Reserve Bank of India (RBI) has established specific regulations covering banking, remittances, and taxation as per the RBI guidelines on NRI accounts.

Banking Options Available to Overseas Indians

Individuals residing abroad are permitted to open designated bank accounts in India for managing income, savings, and investments. These accounts are governed by RBI regulations and include:

Non-Resident External (NRE) Accounts

Non-Resident Ordinary (NRO) Accounts

Foreign Currency Non-Resident (FCNR) Accounts

Each account type serves a distinct purpose and operates under different repatriation and tax conditions.

Rules Governing NRE Accounts

An NRE account is used to manage income earned outside India and is maintained in Indian Rupees. Funds held in this account, including interest, are freely repatriable.

Permitted transactions include:

Transfers to accounts held in the account holder’s name in India

Repatriation of funds to overseas bank accounts

Investments in India, subject to RBI guidelines

Donations to charitable organisations in India

These accounts can be jointly held with another non-resident.

Regulations Applicable to NRO Accounts

NRO accounts are designed for managing income earned within India, such as rent, dividends, pensions, or capital gains. Funds are maintained in Indian Rupees and are subject to repatriation limits.

Permitted uses include:

Local payments such as bills, rent, and taxes

Investments permitted under RBI norms

Donations to charitable institutions

Transfers to self-held accounts in India

Repatriation from these accounts is restricted and requires regulatory compliance.

FCNR Account Guidelines

FCNR accounts are term deposit accounts maintained in foreign currency. These deposits protect account holders from exchange rate fluctuations and allow full repatriation in the same currency.

Permitted activities include:

Repatriation of principal and interest without conversion

Investments in India as permitted by RBI

Difference Between NRE and NRO Accounts

Purpose: NRE accounts manage overseas income, while NRO accounts handle income generated in India.

Repatriation: Funds in NRE accounts are freely repatriable. Transfers from NRO accounts are restricted and regulated.

Tax Treatment: Interest on NRE accounts is exempt from Indian tax, whereas interest earned on NRO accounts is taxable.

Currency: Both accounts are maintained in Indian Rupees, but the source of funds differs.

Joint Holding: NRE accounts can be held jointly with another non-resident, while NRO accounts allow joint holding with a resident Indian as well.

Taxation Framework for Overseas Indians

Tax liability depends on residential status as defined under Section 6 of the Income-tax Act. An individual is treated as a resident if they:

Stay in India for 182 days or more during the previous year, or

Stay for 60 days in the previous year and 365 days in the four preceding years

Certain exceptions apply to Indian citizens visiting India or individuals earning high income but not liable to tax elsewhere.

Tax Implications in India

Income earned in India: Taxable

Income earned abroad: Not taxable

TDS: Higher rates apply compared to residents

DTAA: Relief available to avoid double taxation

Return filing: Mandatory if income exceeds exemption limits or includes capital gains

These compliance requirements form an essential part of NRI account rules in India.

Is a Student Studying Abroad Treated as a Non-Resident?

A student pursuing education outside India is generally classified as non-resident if their stay abroad exceeds the prescribed limits under the Income-tax Act. Residential status is determined solely by physical presence in India during the financial year.

Related Reading

Understanding the distinction between non-resident and person of Indian origin (PIO) status helps overseas Indians comply better with banking and tax regulations.

When it comes to Indians living abroad, the terms NRI and PIO are often used interchangeably, but they have distinct meanings. Understanding the NRI and PIO full form and their differences is essential for anyone planning to live, work, invest, or travel between India and other countries. In this article, we’ll break down the key differences, benefits, and features of NRI and PIO status, helping you make informed decisions.

NRI and PIO Full Form

NRI full form: Non-Resident Indian

PIO full form: Person of Indian Origin

Knowing the nri and pio full form helps clarify eligibility, legal rights, and financial benefits for Indians living overseas or foreign nationals of Indian descent.

Difference Between NRI and PIO

Non-Resident Indian (NRI)

An NRI is an Indian citizen who resides outside India for work, education, or personal reasons. Legally, an individual is considered an NRI if they spend less than 182 days in India in a financial year or 365 days in the preceding four years.

Key features of NRI status include:

Investment eligibility: NRIs can invest in Indian stock markets, mutual funds, and real estate. Some investments may have regulatory restrictions, and taxation applies on Indian-sourced income.

Banking options: NRIs can open Non-Resident External (NRE) and Non-Resident Ordinary (NRO) accounts to manage foreign and Indian income.

Voting rights: NRIs cannot vote in Indian elections.

Repatriation: NRIs can transfer funds earned in India to their country of residence, subject to RBI regulations.

Person of Indian Origin (PIO)

A PIO is a foreign national who can prove their Indian heritage through birth, ancestry, or marriage. Typically, PIOs have at least one parent or grandparent of Indian origin. They are eligible for a PIO Card, which allows long-term travel to India without a visa for up to 15 years.

Key features of PIO status include:

Visa-free travel: PIOs can enter and exit India multiple times without a visa using a PIO Card.

Investment eligibility: PIOs can invest in Indian markets without restrictions.

Banking benefits: PIOs can open NRE accounts to hold and transfer income earned outside India in Indian currency.

Voting rights: Unlike NRIs, PIOs may be eligible to vote if they acquire Indian citizenship.

NRI vs. PIO: Key Differences

Feature

NRI

PIO

Citizenship

Indian citizen

Foreign citizen of Indian origin

Visa Requirement

Yes, unless holding OCI

No (via PIO Card)

Investment Restrictions

Yes, some restrictions apply

No restrictions

Voting Rights

No

Yes, if an Indian citizen

Banking Options

NRE & NRO accounts

NRE accounts

Understanding the difference between NRI and PIO ensures better planning for financial, legal, and personal matters.

1. What is the NRI and PIO full form? The NRI and PIO full form is Non-Resident Indian (NRI) and Person of Indian Origin (PIO). NRIs are Indian citizens living abroad, while PIOs are foreign citizens with Indian ancestry.

2. What is the difference between NRI and PIO? The difference between NRI and PIO lies in citizenship and benefits. NRIs are Indian citizens residing outside India, whereas PIOs are foreign nationals of Indian origin. NRIs have certain investment restrictions, while PIOs can invest freely in India.

3. Who qualifies as NRI and PIO Indian origin? Anyone holding Indian ancestry qualifies as NRI and PIO Indian origin. NRIs must be Indian citizens living abroad, and PIOs are foreign nationals with at least one Indian parent, grandparent, or spouse.

4. Can NRI and PIO Indian origin invest in India? Yes, both NRI and PIO Indian origin individuals can invest in Indian markets. NRIs have some restrictions on real estate and taxation, while PIOs can invest without limitations.

5. Do NRIs and PIOs have voting rights in India? NRIs cannot vote in Indian elections unless they acquire a valid voting card in India. Some PIO Indian origin individuals may vote if they gain Indian citizenship.

6. What are the banking options for NRI and PIO Indian origin? Both NRIs and PIO Indian origin individuals can open NRE accounts. NRIs can also open NRO accounts to manage income earned in India, while PIOs primarily use NRE accounts.

7. How long can PIOs stay in India without a visa? PIOs, as persons of Indian origin, can enter and exit India without a visa for up to 15 years using a PIO card, making travel convenient compared to NRIs.

8. Where can I find official rules for NRI and PIO Indian origin? You can check the latest regulations on Ministry of External Affairs – PIO/NRI Guidelines for accurate details on eligibility, benefits, and investments.

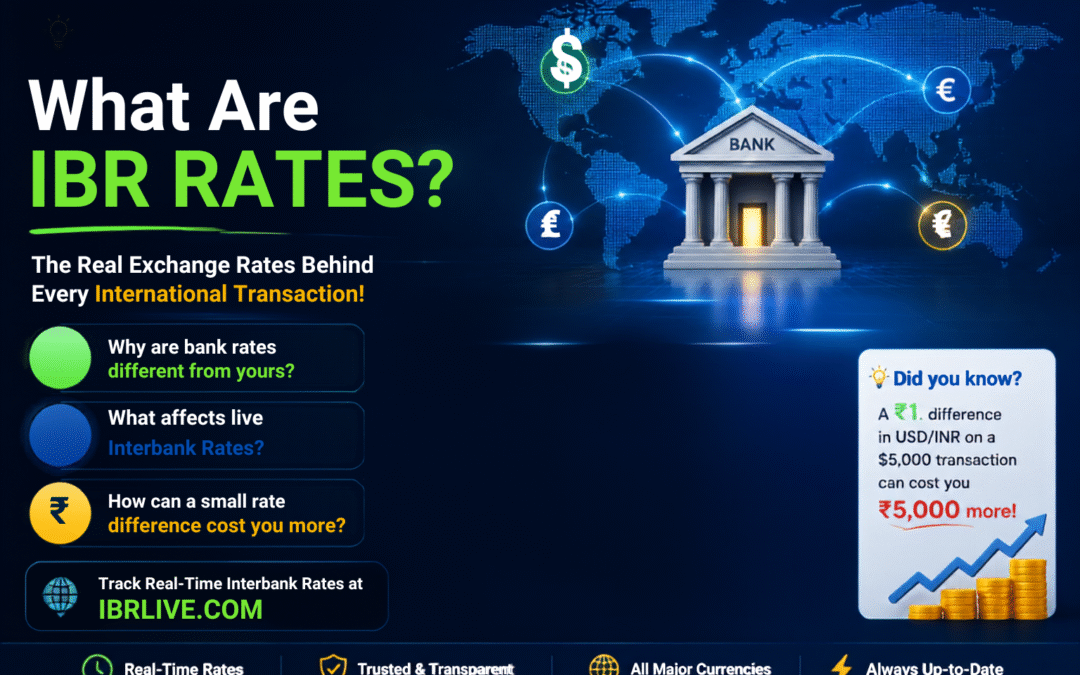

What Are IBR Rates? Meaning, Live Interbank Exchange Rate & Why They Matter

IBR Rates, also known as Interbank Exchange Rates, are the real-time foreign exchange rates at which banks trade currencies with each other in the global forex market. These rates are considered the benchmark exchange rates for international currency transactions and are widely used by banks, financial institutions, importers, exporters, and forex platforms worldwide.

For example, the IBR rate for USD refers to the live exchange rate at which banks exchange the United States Dollar against the Indian Rupee or other currencies in the interbank market.

Businesses and individuals closely monitor Interbank Rates because they directly impact:

International money transfers

Import-export payments

Forex card pricing

Foreign currency exchange

Overseas education payments

Travel expenses

What are IBR Rates (Interbank Exchange Rates)?

The interbank exchange rate is the exchange rate at which banks buy and sell currencies among themselves. These rates are usually available only to banks and large financial institutions because they involve high-volume forex transactions.

IBR Rates are also known as:

Spot Rates

Interbank Forex Rates

Wholesale Forex Rates

Live Market Exchange Rates

The interbank market is the world’s largest financial market, where global banks continuously trade currencies like:

United States Dollar

Euro

British Pound Sterling

Japanese Yen

Australian Dollar

Canadian Dollar

These rates change every second depending on global market demand and supply.

How Do Interbank Rates Work?

The interbank market is one of the world’s largest financial markets, where global banks continuously trade currencies like United States Dollar, Euro, and British Pound Sterling. According to the Bank for International Settlements, the global forex market trades trillions of dollars daily.

When banks need foreign currencies for international settlements, they buy and sell currencies from each other through the interbank forex market.

For example:

One bank may need USD for import payments.

Another bank may have excess USD liquidity.

The exchange takes place at the prevailing Interbank Exchange Rate.

These transactions happen electronically in real time across global forex trading networks.

The rates are quoted with:

Bid Price → the rate at which banks buy currency

Ask Price → the rate at which banks sell currency

The small difference between these prices is called the spread.

How Are Interbank Rates Determined?

IBR Rates are determined primarily by supply and demand in the global foreign exchange market.

Several factors influence Interbank Exchange Rates:

1. Economic Data

Economic indicators such as:

inflation

GDP growth

employment data

trade balance

can significantly impact currency demand.

2. Central Bank Policies

Interest rate decisions by central banks strongly affect currency movements.

For example:

RBI policies affect INR movement.

US Federal Reserve policies impact the interbank dollar rate globally.

3. Political Events

Elections, geopolitical tensions, trade wars, and government policies can create volatility in forex markets.

4. Global Market Sentiment

Investor confidence and global risk appetite also influence currency demand.

Why Do Interbank Rates Change Every Second?

Unlike fixed exchange rates, Interbank Exchange Rates are dynamic.

Currencies are traded 24 hours a day across:

London

New York

Singapore

Tokyo

Hong Kong

As millions of forex transactions happen globally, Rates continuously fluctuate based on:

market liquidity

global demand

economic news

institutional trading activity

Live Example:

Suppose the live interbank dollar rate is:

USD/INR = ₹96.8302

A retail customer may receive:

₹97.80 to ₹99.50 for forex card loading or currency exchange after bank markup.

This difference occurs because banks and forex providers add:

operational charges

risk buffers

profit margins

For example, if a student or traveler exchanges $5,000:

At the live Interbank Exchange Rate of ₹96.8302, the total cost would be approximately ₹4,84,151.

At a retail forex rate of ₹98.00, the total cost becomes ₹4,90,000.

That’s a difference of nearly ₹5,849 due to markup over the live interbank rates.

This is why businesses, importers, exporters, students, and travelers closely monitor the interbank dollar rate and real-time exchange rate for usd before making international payments.

Difference Between Interbank Exchange Rates and Forex Card Rates

Feature

IBR Rates

Forex Card Rates

Used By

Banks & Institutions

Retail Customers

Margin

Very Low

High

Market Type

Wholesale Forex Market

Retail Forex Market

Real-Time

Yes

Often Marked Up

Spread

Minimal

Wider

Best For

Large Forex Transactions

Travel Spending

While these Rates reflect the actual market value of a currency, Forex Card Rates include additional bank margins.

For example, banks like ICICI Bank display their own retail forex card pricing, which is usually higher than the live Interbank Exchange Rate.

Many people ask why customers cannot access the same rates banks receive.

The reason is that banks add margins to cover:

currency fluctuation risks

operational costs

payment processing

liquidity management

profit margins

Retail customers usually receive marked-up exchange rates compared to the wholesale interbank market.

Why Are Interbank Rates Important?

1. International Money Transfers

When businesses or individuals send money internationally, exchange rates directly impact the final amount received.

Better exchange rates can save substantial costs on:

tuition fee payments

import payments

overseas transfers

business remittances

2. Importers and Exporters

Import-export businesses monitor the Rates daily because even small forex fluctuations can significantly impact profit margins.

For example:

Importers prefer a stronger INR.

Exporters benefit from a weaker INR.

3. Forex Market Benchmarking

The Interbank Exchange Rate acts as the benchmark rate for:

banks

forex companies

remittance providers

travel card providers

4. Economic Impact

Currency strength affects:

exports

imports

inflation

foreign investments

trade competitiveness

A stronger domestic currency can make exports more expensive globally.

Difference Between Google Exchange Rate and Interbank Rates

Google exchange rates are generally mid-market reference rates collected from financial data providers.

However, actual Interbank Exchange Rates can differ slightly because:

forex markets move continuously

banks trade at different bid-ask spreads

liquidity conditions vary

The live interbank dollar rate changes every second during active forex trading hours.

Where Can You Find Authentic & Real-Time Rates?

Many websites display currency exchange rates, but not all provide authentic real-time Interbank Exchange Rates.

A reliable source should provide:

live forex market updates

real-time interbank pricing

multi-currency support

transparent exchange rates

generally look for real-time wholesale forex market pricing.

Common Use Cases

IBR Rates are widely used for:

International wire transfers

Import-export settlements

Forex trading

Currency risk management

Overseas education payments

Travel planning

Treasury operations

Global business payments

FAQs About IBR Rates

What is an Interbank Exchange Rate?

An Interbank Exchange Rate is the rate at which banks exchange currencies with each other in the wholesale forex market.

Is IBR Rate the Same as Spot Rate?

Yes, IBR Rates are commonly referred to as spot exchange rates because they represent real-time market pricing for immediate currency settlement.

What is the interbank dollar rate?

The interbank dollar rate refers to the live wholesale exchange rate for the United States Dollar in the interbank forex market.

Why are Forex Card Rates higher than IBR Rates?

Forex card providers and banks add margins over Interbank Exchange Rates to cover operational costs and currency risks.

Can individuals get Interbank Rates?

Retail customers usually do not receive exact Interbank Exchange Rates because banks apply markups and spreads on retail forex transactions.

Why do Interbank Rates fluctuate constantly?

IBR Rates change continuously due to:

global forex trading activity

economic news

central bank decisions

market demand and supply

Conclusion

Interbank Rates play a critical role in the global foreign exchange ecosystem. These live Interbank Exchange Rates serve as the benchmark for international currency trading and influence everything from import-export transactions to travel forex cards and international remittances.

Understanding how IBR Rates work can help businesses and individuals make smarter forex decisions, reduce currency conversion costs, and better understand global market movements.

Whether you are tracking the interbank dollar rate, searching for the latest ibr rate for usd, or comparing forex card pricing, knowing the difference between retail exchange rates and live Interbank Exchange Rates is essential in today’s global economy.

A forex card rate is like a display board where a bank publishes exchange rates for buying and selling foreign currencies, travel cards, and currency notes. The spread between buying and selling currencies in a card rate is generally kept very wide. For example, SBI forex card rates for USD/INR can be in the form of the below-mentioned table:

Currency

Bank Buying Rate

Bank Selling Rate

TT Buying rate

Bills Buying rate

Currency notes

Travel card

Traveller’s cheques

TT Selling rate

Bills Selling rate

Currency notes

Travel card

Traveller’s cheques

Demand draft

United States Dollar (USD)

80.94

80.94

79.45

80.69

80.69

84.58

84.58

85.94

84.36

84.36

84.24

When a bank displays a card rates for foreign exchange, it may show both the TT buy rate and the TT sell rate. The TT buy rate is the rate at which the bank will buy foreign currency from the customer in exchange for local currency. The TT sell rate is the rate at which the bank will sell foreign currency to the customer in exchange for local currency. The difference between the TT buy and TT sell rates is known as the bid-ask spread, and it represents the bank’s profit margin for facilitating the transaction. The bid-ask spread can vary depending on various factors, such as market conditions, currency volatility, and the size of the transaction. Customers need to understand the Bank’s card rate and the bid-ask spread to make informed decisions about foreign exchange transactions and to minimize the costs associated with such transactions.

Do the Forex Card Rate of each bank differ?

The Fx Card Rates can differ across banks. Each bank sets its own exchange rates based on a variety of factors, such as its cost of acquiring foreign currency, operating expenses, and profit margin. For Example HDFC Bank Forex Rates for USD/INR may differ with ICICI Bank Forex Rates and SBI Forex Card Rates Today.

The differences in Foreign Exchange Card Rates across banks can impact the cost of foreign exchange transactions for customers. Therefore, comparing the fx card rates offered by different banks before making a foreign exchange transaction is essential to get the best possible rate.

What is the difference between the Forex Card Rate & Interbank Exchange Rate?

The Forex card Rate vs Interbank Exchange Rate are two different rates used in foreign exchange transactions. The main differences between the two are:

Definition: The Interbank Exchange Rate is the rate at which banks buy and sell currencies with each other in the wholesale market. It is used by banks to settle their transactions and by other financial institutions as a benchmark for pricing their foreign exchange products.

On the other hand, the foreign exchange card rate, refers to the rate derived on a daily basis by bank based on the Interbank Exchange Rate by keeping a substantial margin on buy and sell foreign exchange transactions. Generally the margin loaded in card rate is more than 1 rupee on USD/INR transactions, 2 rupee on EUR/INR transactions and 3 Rupee on GBP/INR transactions. This margin can vary across banks based on their different strategies and other market factors.

Calculation: Numerous economic considerations and market dynamics of supply and demand as well as market dynamics of supply and demand, influence the Interbank Exchange Rate. While the bank’s profit margin, the interbank rate, and any other fees or charges are all included in the Bank’s Card Rate, which is established by the bank.

Spread: The difference between a currency pair’s purchasing and selling rates for a currency pair is known as the bid-ask spread. Due to banks’ high volume of transactions, the spread for Interbank Exchange Rate is normally quite small, with only a few pips. For example the spread between USD to INR IBR rate for hdfc bank forex exchange rates today may be 1 to 3 paisa only. As a result of the bank’s profit margins and other expenses related to supplying retail consumers with foreign exchange services, the gap in Fx card rate is often greater and can range between 1 to 3 Rupees.

Source: Card Rates can be found on specific bank’s website for Example ICIC Bank Forex Card Rates can be found on link available on ICICI Bank’s official website. Whereas Interbank Rates ca be found on the most trusted forex website ibrlive.com.