by sohamkumar245 | Dec 27, 2025 | Exchange Rate API

Why Exchange Rate APIs Are The Quiet Engine Behind Fintech: An Introduction

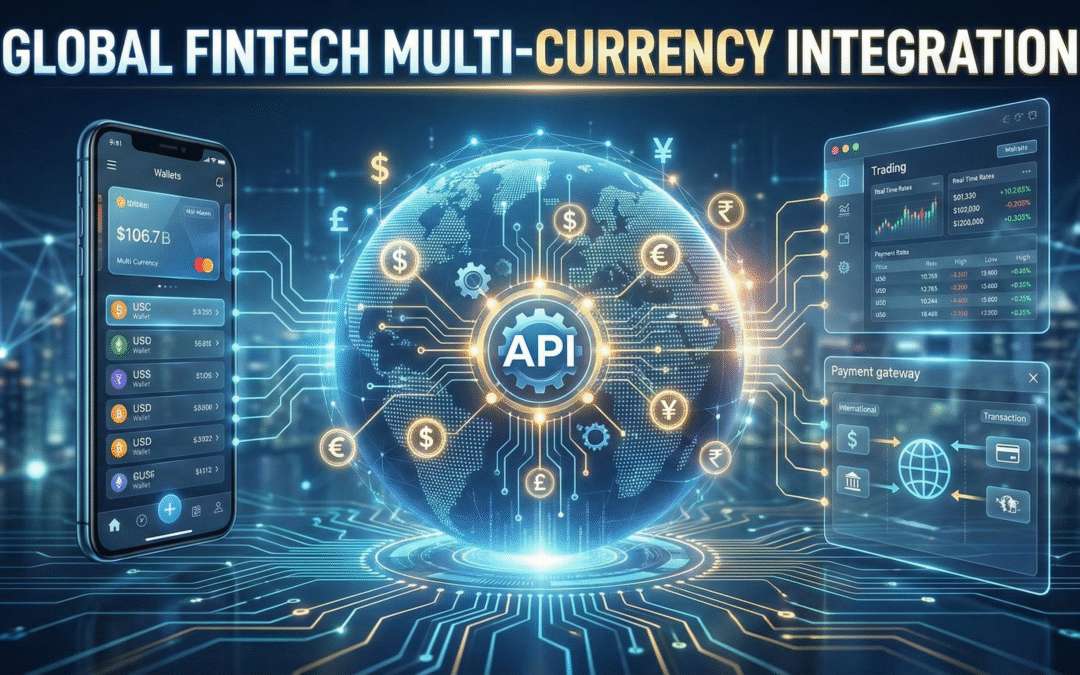

Imagine this: you’re in Paris, and you’re using Apple Pay to pay for coffee on your phone. Your bank account back home is in INR, yet the transaction goes through right away in euros. Have you ever thought about what makes that magic happen?

The answer is exchange rate API for cross-border payments that work in the background.

Publishing correct currency conversion rates is not a nice thing for fintech companies that handle cross-border payments; it’s a matter of life and death. Customers want to know what’s going on; they want to see the current exchange rate before they agree to anything. Without it, trust goes down and conversion goes down.

APIs make sure such numbers aren’t just guesses. They give you real-time exchange rates, money converter tools, and even help businesses keep up with the rules. And even though there are big firms all over the world in this field, IBRLIVE stands out because it offers speed, accuracy that is first in INR, and RBI alignment for fintechs that work in India.

The Growth of Multi-Currency Needs

Fintech is growing quickly around the world. The World Bank says that remittances reached $860 billion in 2022, with India receiving the most. Meanwhile, mobile payments are still growing around the world. Apple Pay and the Google Pay app conduct billions of transactions every year.

What is the challenge?

Customers don’t simply want things to be easy; they also want them to be clear. No secret spreads. No promises that aren’t clear. When financing a university in the U.S. or transferring money to family abroad, they want to know exactly how much ₹10,000 will turn into. That’s why currency conversion APIs are so important to new ideas in fintech.

- Use Instant Money Converters Powered by Exchange Rate APIs

Have you ever looked for a “money converter” before going on a trip?

APIs make that work. XE and Wise are two fintech apps that use currency exchange rate APIs to give users real-time conversions. This makes sure that clients always see the best euro exchange rate or USD/INR value before making a decision.

Evidence: Wise handles more than £9 billion in cross-border payments every month, using clear APIs to uphold its promise of “mid-market rates”.

- Clear cross border payments

Hidden fees are the worst thing for fintech. APIs enable companies display accurate rates for cross-border payments, which makes sure they follow rules about openness.

The World Bank often talks about how important it is for remittances to have clear disclosures in order to lower costs for consumers.

- Mobile wallets are becoming popular all over the world.

When people use Apple Pay or the Google Pay app to pay for things in other countries, APIs take care of the conversion in the background. Without this, fintechs run the danger of losing clients who are unhappy with unexpected fees.

Evidence: PayPal uses real-time APIs at checkout to make it easier to understand foreign exchange rates, which lowers the number of people who leave their carts.

- Changing Prices in Travel and E-Commerce

Have you ever seen Amazon show you prices in your own currency?

That’s how APIs work. Booking.com and other travel companies use APIs to figure out how much tickets cost based on today’s currency rate. This makes things more clear and cuts down on drop-offs.

- Wallets and accounts that work with more than one currency

Fintech companies that shake things up, like Revolut, let consumers keep more than 30 currencies and convert them right away at real rates. This function is powered by APIs, which provide users peace of mind that they are obtaining the best euro or USD/INR conversion rate in the app.

- Digital kiosks are taking the place of paper rate boards.

There was a time when banks used chalkboards to display how much money was worth. AD II forex companies and FFMCs in India now use APIs like IBRLIVE to show live foreign exchange rates on websites and applications. This looks professional and meets RBI’s criteria for compliance.

- Managing Risk and the Corporate Treasury

Companies that do business around the world use APIs for hedging and forward contracts. Real-time data goes straight to treasury dashboards. Global APIs like OANDA provide you a lot of options, while IBRLIVE offers accuracy that Indian businesses need.

- Working with payment gateways

Stripe and PayPal are two examples of payment gateways that employ currency exchange APIs to manage settlements in more than one currency. Fintech firms can use this model with providers like IBRLIVE, which makes it easy for Indian enterprises to grow and do business around the world.

- Apps and charts for the financial market

Trading applications use APIs to connect to sites like TradingView so that you may see live charts of currency trading or FX EUR/USD. This characteristic draws in retail traders who want accuracy down to the second.

- Reporting, auditing, and following the rules

APIs also take care of the dull but important part: compliance. The rules set by the RBI and the ECB say that companies must report correct exchange rates. APIs give you verified currency rates with timestamps, which makes audit trails easy to follow.

Best Ways to Integrate Exchange Rate API

So, how do you add an exchange rate API to a finance software without destroying anything?

Here are some best practices for integrating a financial exchange rate API:

- Keep things simple: use REST APIs that return JSON.

- Make it safe: Always use HTTPS and keys to log in.

- Plan for downtime: save data in a cache and have backup providers. If you don’t, it’s like trading forex without a stop-loss.

- Measure of performance: Check uptime (99.9% or above is required) to see how well it works.

- Compliance: Make sure your provider follows the rules set by regulators like the RBI.

Why IBRLIVE is Good for Fintechs

Sure, Currencylayer and OANDA are amazing worldwide APIs. But when it comes to AD II forex companies, Fintechs or FFMCs in India, IBRLIVE is the best:

- Local Accuracy: Rates that emphasis on INR that global APIs don’t give as much weight to.

- Speed: With a latency of less than a second, clients always see new values.

- Compliance: Unlike other providers, this one is made to work with RBI.

- Developer-Friendly: Easy to understand docs, simple onboarding, and simple REST calls.

IBRLIVE helps fintechs globally by providing accurate Exchange Rate API for Cross-Border Payments but it provides an edge to companies who are based in India but want to grow internationally by bridging the gap between local compliance and international performance.

FAQs

Q1: What’s the simplest approach for fintechs to let customers know about exchange rates?

A: Use an API-powered money converter or currency exchange rate widget like IBRLIVE.

Q2: Do APIs work with mobile payment apps like Google Pay and Apple Pay?

A: Yes. APIs make sure that conversions happen right away, which stops hidden fees.

Q3: How do fintech companies give their consumers the best euro exchange rate?

A: By selecting BRLIVE API for fintech companies that offer clear, mid-market rates with no extra costs.

Q4: What are the best ways to integrate a financial exchange rate API?

A: REST/JSON integration, caching, redundancy, secure endpoints, and checks for compliance with providers.

by Neha Sharma | Mar 6, 2025 | Blog

In today’s interconnected global economy, staying updated with live currency exchange rates is paramount, especially when dealing with the ever-fluctuating dynamics between the US dollar and the Indian rupee. For those seeking real-time insights into the dollar to rupee live exchange rate, IBRLive emerges as the ultimate solution, offering unparalleled accuracy and reliability without the dreaded 60-second delay commonly found elsewhere like on Xe.

Dollar to Rupee Live Rates: Their Significance

For those involved in global trade, investments, and financial transactions, both individuals and businesses, the dollar to rupee live exchange rate is crucial. One of the most frequently traded currency pairs worldwide, changes in the USD/INR rate can have a significant impact on several different economic sectors.

-

International Trade:

For businesses involved in importing and exporting goods and services between the United States and India, the dollar to rupee live exchange rate directly impacts the cost of transactions. A favorable exchange rate can enhance competitiveness in international markets, while unfavorable rates may lead to increased costs and reduced profitability.

-

Investment Opportunities:

Investors and financial institutions closely monitor the dollar to rupee exchange rate to identify lucrative investment opportunities. A strengthening rupee relative to the dollar may attract foreign investment inflows into India, stimulating economic growth and capital formation. Conversely, a depreciating rupee may prompt investors to reconsider their investment strategies and asset allocation.

-

Economic Indicators:

A vital sign of the general stability and well-being of the Indian economy is the exchange rate between the US dollar and the Indian rupee. To evaluate variables like inflation, trade balances, the efficacy of monetary policy, and external vulnerabilities, central banks, decision-makers, and market analysts examine changes in exchange rates. Variations in the USD/INR exchange rate can impact macroeconomic policies and forecasts.

IBRLive: Your Trusted Source for Real-Time Exchange Rates(dollar to rupees exchange rate live)

In the dynamic landscape of currency markets, having access to live exchange rates is essential for making informed decisions and managing currency-related risks effectively. IBRLive emerges as the preferred choice for individuals and businesses seeking reliable and accurate dollar to rupee live rates. IBRLive sets itself apart by providing live currency exchange rates without any 60-second delay, ensuring users have access to the most current and accurate information at their fingertips. With IBRLive, you can make informed decisions swiftly, reacting promptly to market fluctuations and maximizing your financial outcomes.

With IBRLive users benefit from:

Instant Updates:

Stay updated with real-time exchange rate fluctuations, enabling timely decision-making and execution of currency transactions.

User-Friendly Interface:

IBRLive’s intuitive platform provides easy navigation and access to a wealth of currency-related information, empowering users to track exchange rates effortlessly.

Comprehensive Coverage:

IBRLive offers coverage of a wide range of currency pairs, including the dollar to rupee (USD/INR) pair, ensuring users have access to the latest exchange rate data for their currency needs.

Reliability and Accuracy:

IBRLive prides itself on delivering accurate and reliable exchange rate information, with no 60-second delay, allowing users to trust the data and insights provided.

Customizable Features:

IBRLive offers customizable features such as rate alerts, historical data analysis, and currency conversion tools, catering to the diverse needs of individual users and businesses.

Introducing Fxpress Standard: Your Gateway to Live Interbank Exchange Rates(dollar to rupees exchange rate live)

At the core of IBRLive’s offerings lies Fxpress Standard, a robust product designed to meet the diverse needs of individuals and businesses alike. Let’s delve into some of its key features:

Live Interbank Exchange Rates:

Fxpress Standard offers access to real-time interbank exchange rates, allowing users to track the dollar to rupee live rates with unparalleled precision.

Cash Tom Spot Rates:

Stay updated with cash Tom Spot rates, facilitating seamless transactions and reducing uncertainty in currency exchanges.

Monthly & Broken Date Forward Rates:

Plan and mitigate risks by accessing monthly and broken date forward rates, empowering you to make strategic financial decisions.

Currency Forecast:

Gain valuable insights into future currency trends with Fxpress Standard’s currency forecasting capabilities, enabling proactive decision-making.

Currency Calculator:

Calculate conversions effortlessly with IBRLive’s intuitive currency calculator, simplifying complex currency exchanges.

Historical Rates:

Access historical exchange rate data to analyze trends and effectively inform your future strategies.

Day Opening and Closing SMS:

Receive timely notifications regarding day opening and closing rates via SMS, ensuring you’re always in the loop.

Forward Contract Management Tool:

Manage forward contracts efficiently and mitigate currency risk with IBRLive’s comprehensive management tool.

Set personalized rate alerts and receive notifications when your desired exchange rate is reached, empowering you to seize favorable opportunities.

RPC & PCFC Management Tool:

Streamline RPC (Resident Foreign Currency) and PCFC (Pre-Shipment Credit in Foreign Currency) management with IBRLive’s dedicated tool, optimizing your financial operations.

One-Time FX Rate Negotiation with the Bank:

Simplify negotiations with banks by leveraging IBRLive’s one-time FX rate negotiation feature, ensuring favorable terms and conditions.

RPC & PCFC ROI Negotiations:

Maximize returns on RPC and PCFC investments through effective negotiations facilitated by IBRLive’s expertise and insights.

Conclusion IBRLive stands as the epitome of reliability and accuracy in live currency exchange rates, offering users access to real-time information without the 60-second delay typically encountered elsewhere. With Fxpress Standard, users access a comprehensive suite of features designed to streamline currency exchange processes and optimize financial outcomes. Whether you’re seeking to make timely currency conversions or a business looking to hedge against currency risks, IBRLive and Fxpress Standard provide the tools and insights necessary to navigate the complex world of currency exchange with confidence and precision. Choose IBRLive today and experience the difference firsthand.

by Deepak Madan | Mar 6, 2025 | Blog

What Is a Currency Forward Contract?

A currency forward contract can be defined as buying or selling a specific currency at a specified future price for delivery on a specified future date.

Who Can Book a Currency Forward Contract?

Any importer or exporter having exposure to foreign currency can book a forward contract with its bank based on underlying (purchase order or pro forma invoice) to hedge his currency movement risk.

How to Book a Currency Forward Contract?

Step 1: On request, the bank set up a forward booking limit on behalf of its client. To set up the forward booking limit bank demands a fixed deposit of approx. 5% of your total booking requirements in the INR term. For example, if you want to book USD100000 then you will have to produce a fixed deposit of Rs. 375000.00 to your bank (considering USD/INR at 75.00). If you are a credit customer then the bank may also set up the limit based on your collateral mortgaged with the bank.

Step 2: You must produce an underlying (valid purchase order or pro forma invoice) mentioning the delivery and payment terms before your bank to book a currency forward contract.

Step 3: The Bank gives you a forward rate and with your consent, book the same. For example, if you want to book USD 100000 for delivery after the end of 3 months. Considering the current USD to INR spot rate of 75.00, the bank may give you a forward rate of 75.90. Here 0.90 is the premium for three months. Please note that exporters get the benefit of premium and importers have to pay the premium because USD is almost on premium in comparison to INR. You may refer to ibrlive.com for live forward rates.

Step 4: On successful booking of the contract bank agrees, generally on a 100 Rs. Stamp paper. The agreement contains all details of the contract and it is signed by both the bank and the client.

How Currency Forward Contracts Are Utilized?

On successful arrival of payment against export or sending the payment for import on the maturity date of the forwarding contract, the bank gives you the same rate which was booked earlier under the forwarding contract irrespective of the current spot rate on the maturity date.

A forward contract can be utilized for other payments irrespective of the underlying (purchase order or pro forma invoice) on behalf of which it was booked.

Early utilization of forwarding contracts is also possible if your payment has come earlier than the expected date.

Where to Check Exact Forward Premiums and Forward Rates?

Many websites show the month-wise or broken date forward rates for a subscription basis. You may refer to ibrlive.com to know the exact premiums and final forward rate, even for broken dates.

Advantages of Currency Forward Contract

For importers & exporters, the main advantage of booking a currency forward contract is to hedge their foreign currency exposure from adverse movements.

Exporters booking a forward contract for USD to INR, EUR to INR, GBP to INR, or any major currency benefit from a premium added to the present spot rate.

Can I Cancel a Forward Contract?

Yes, the forward contract can be cancelled on the maturity date or 3 days after the maturity date. Cancellation is done on a spot rate and any profit or loss will be passed on to the customer if the same is cancelled on or before the maturity date.

If the forward is cancelled any day between the 3 days grace period, then the profit will not be passed on to the customer but any loss will be recovered from his account.

A forward contract can also be cancelled before the maturity date. Apart from profit & loss calculation from spot day, the client will also have to forgo extra premium from the date of cancellation to maturity.

by Nancy Thakur | Mar 2, 2025 | Blog

Introduction

Explore the world with ease as Indian passport holders enjoy access to a variety of Indian Passport Visa Free Countries and Visa on arrival countries for Indians. Discover the growing list of E Visa countries for Indian passport holders and stay updated on the India passport rank. Travel hassle-free with information on free visa for Indians and plan your next international adventure.

In a world where borders define opportunities, the strength of a passport becomes a crucial determinant of one’s ability to explore and experience different cultures. The Indian passport, held by over 1.4 billion citizens, has steadily grown in its global ranking, offering increasing access to various countries without the need for a visa or with simplified visa processes. This blog explores the power of the Indian passport, detailing the countries where Indians can travel visa-free, obtain a visa on arrival, or apply for an e-visa.

Understanding Passport Strength

The strength of a passport is typically measured by the number of countries its holders can enter without a visa or with a visa on arrival. The Indian passport, while not among the top tier globally, still provides access to a significant number of destinations, reflecting India’s growing diplomatic relationships and its citizens’ global presence.

Indian passport rank

As of August 2024, the India passport rank is 82nd on the Henley Passport Index. This ranking allows Indian passport holders to travel visa-free to 58 countries, including popular destinations like Indonesia, Maldives, and Thailand.

Discover the Wonders of India Visa-Free Countries

Exploring Indians’ visa-free countries not only simplifies travel but also opens a world of opportunities for cultural exchange and adventure without the hassle of lengthy visa applications. Indian passport holders can visit the following countries offering free visas for Indians:

- Barbados

- Bhutan

- Dominica

- El Salvador

- Fiji

- Grenada

- Haiti

- Indonesia

- Jamaica

- Mauritius

- Micronesia

- Nepal

- St. Kitts and Nevis

- Senegal

- Serbia

- Trinidad and Tobago

- Tunisia

- Vanuatu

These destinations not only offer a seamless entry process but also boast rich cultural heritage, stunning landscapes, and unique experiences that make them attractive for Indian travelers.

Visa on arrival countries for Indians

For countries that don’t offer visa-free entry, many provide the option to obtain a visa upon arrival. This system simplifies the travel process, as it eliminates the need for advance visa applications, making spontaneous travel more feasible. Indian passport holders can avail themselves of this facility in the following countries:

- Bolivia

- Cambodia

- Cape Verde

- Comoros

- Ethiopia

- Gabon

- Guinea-Bissau

- Guyana

- Iran

- Jordan

- Kenya

- Laos

- Madagascar

- Malawi

- Maldives

- Mauritania

- Mozambique

- Myanmar

- Palau

- Rwanda

- Samoa

- Seychelles

- Somalia

- Sri Lanka (Electronic Travel Authorization)

- St. Lucia

- Tanzania

- Thailand

- Togo

- Tuvalu

- Uganda

- Zimbabwe

These countries present diverse opportunities, from the tropical beaches of the Maldives and Seychelles to the cultural riches of Iran and Jordan.

E Visa countries for Indian passport holders

The advent of e-visas has revolutionized international travel, offering a convenient and efficient way to obtain permission to enter a foreign country. Indian passport holders can apply for an e-Visa from the comfort of their homes for the following countries:

- Armenia

- Azerbaijan

- Bahrain

- Benin

- Colombia

- Cote d’Ivoire (Ivory Coast)

- Djibouti

- Georgia

- Guinea

- Kyrgyzstan

- Lesotho

- Moldova

- Montenegro

- Oman

- Papua New Guinea

- Qatar

- Sao Tome and Principe

- Singapore

- South Korea

- Suriname

- Uzbekistan

- Zambia

The e-visa process is typically straightforward, requiring basic information, a valid passport, and fee payment. It saves time and offers peace of mind before starting your journey.

The Increasing Influence of the Indian Passport

The growing list of visa-free nations for India, visa-on-arrival, or e-visa access to Indian passport holders is a testament to India’s rising global influence. It reflects the country’s strong diplomatic ties and the recognition of Indian travelers’ contributions to international tourism.

For Indian citizens, the ability to travel with fewer visa-related hassles opens up a world of possibilities. Whether it’s exploring the pristine beaches of Fiji, embarking on an adventure in the mountains of Bhutan, or experiencing the vibrant culture of Serbia, the Indian passport is truly a gateway to the world.

Conclusion

The power of the Indian passport is undeniable. With access to a diverse range of countries across continents, Indian travelers have the opportunity to explore the world with relative ease. As India’s global standing continues to rise, the strength of its passport is likely to improve further, unlocking even more destinations for its citizens.

So, if you’re an Indian passport holder, now is the perfect time to start planning your next international adventure. Whether you’re seeking visa-free entry, visa-on-arrival convenience, or the simplicity of an e-visa, the world is waiting for you!

Travel is about freedom, exploration, and discovery. With the Indian passport in hand, these experiences are closer than ever before. Safe travels!

Visit top 10 cheapest countries to travel from India

by Deepak Madan | Mar 1, 2025 | Blog

Investing in companies or assets outside of India is known as overseas direct investment. Overseas Direct Investment (ODI) allows Indian residents, including individuals, firms, and companies, to invest in foreign businesses or projects. What is the limit of ODI investment? Indian entities can invest up to 400% of their net worth abroad, as per RBI regulations.

Who is eligible for ODI? Resident individuals, partnership firms, limited liability partnerships, and companies can undertake ODI, provided they meet the requirements.

What is overseas direct investment? It is a means for Indian entities to expand globally, establish a lasting interest, and tap into international markets.

The following three categories of investments make up an ODI:

- Purchasing equity in any unlisted firm or subscribing to a foreign entity’s memorandum of association.

- An investment of 10% or more of a stated foreign company’s paid-up equity capital.

- An investment that represents less than 10% of a stated foreign company’s paid-up equity capital shall be controlled.

Who is eligible to make ODI?

Investments in entirely owned subsidiaries or joint ventures can be made by public and private limited corporations, partnership companies registered under the Indian Partnership Act of 1932, and limited liability partnerships registered under the LLP Act of 2008. Additionally, residents are able to invest abroad. The LRS allows for investments in mutual funds, foreign securities, real estate, and other assets totaling up to USD 250,000 every fiscal year. The investment must abide by the RBI’s reporting guidelines, which include submitting the appropriate paperwork to the RBI and authorized dealers.

Please note that Sole proprietorship and unregistered partnership entities are not eligible to make ODI in WOS or JVs under automatic route.

Mode of ODI payment?

- Payment mode: The remittance for overseas investments should be made through an Authorized Dealer (AD) bank, which is a bank authorized by the RBI to deal in foreign exchange transactions.

- Purchase of foreign currency: The foreign currency required for overseas investments must be purchased from the AD bank at the prevailing market rate.

- Escrow accounts: The RBI may permit the use of escrow accounts or special accounts in specific cases, subject to certain conditions and safeguards.

- Routing transactions: All transactions related to overseas investments must be routed through the same AD bank, ensuring compliance with the guidelines issued by the RBI.

- ODI in the form of cash is not permitted.

- Indian entities may make remittances to their office or branch abroad only for normal business operations. Hence, No ODI is permitted for investment into the branch offices abroad

Knowledge of the Automatic Route

Any monetary commitment up to USD 1 billion in a financial year does not require prior RBI clearance if the Indian party’s entire commitment falls within the acceptable limit under the Automatic Route (i.e., falls within 400% of net worth as per the most recent audited balance sheet).

The Role of Authorized Dealer Category – I Banks

All transactions related to overseas investments must be routed through the same AD bank, ensuring compliance with the guidelines issued by the RBI.

Components of Financial Commitments

Financial commitments in overseas JVs/WOS consist of equity shares, Compulsorily Convertible Preference Shares (CCPS), other preference shares, loans, guarantees (excluding performance guarantees), and bank guarantees (backed by a counter guarantee/collateral by the Indian party).

- 100% of the number of equity shares and/ or Compulsorily Convertible Preference Shares (CCPS);

- 100% of the number of other preference shares;

- 100% of the amount of the loan;

- 100% of the amount of guarantee (other than performance guarantee) issued by the Indian Party;

- 100% of the amount of the bank guarantee issued by a resident bank on behalf of the Indian Party’s JV or WOS, provided that the bank guarantee is supported by a counter-guarantee or collateral.

- 50% of the amount of the performance guarantee issued by the Indian Party, with the condition that prior Reserve Bank approval must be obtained before sending money beyond the financial commitment’s limit if the outflow resulting from the performance guarantee’s invocation causes it to go over.

Conditions for Investments and Financial Commitments under automatic route

Investments and financial commitments in overseas JVs/WOS must adhere to specific conditions:

- The Indian party/entity may extend loans/guarantees only to overseas JVs/WOS in which it has equity participation. Proposals for financial commitments without equity contributions may be considered by the RBI under the approval route.

- Indian parties should not be on the RBI’s caution list, defaulters list, or under investigation by any investigation/enforcement agency or regulatory body.

- Share valuation must be performed by a Category I Merchant Banker registered with SEBI or an Investment Banker/Merchant Banker outside of India registered with the relevant regulatory authority in the host country for investments exceeding USD 5 million in partial or complete acquisitions.

- When an investment is made through a share swap, the valuation of the shares must be performed by a Category I Merchant Banker registered with SEBI or an investment banker outside of India registered with the relevant regulatory body in the host country.

- In cases where a registered partnership firm invests in an overseas JV/WOS, individual partners may hold shares on behalf of the firm if the host country’s regulations or operational requirements warrant such holdings.

- Indian parties may acquire shares of a foreign company in exchange for ADRs/GDRs, subject to specific conditions.

- Investments in Nepal are permitted only in Indian Rupees. Investments in Bhutan can be made in Indian Rupees or freely convertible currencies. All dues receivable on investments and their sale/winding-up proceeds must be repatriated in freely convertible currencies.

- Investments in countries identified by the Financial Action Task Force (FATF) as “non-cooperative countries and territories” are not permitted. Investments in Pakistan are permissible under the approval route.

Methods of funding for overseas direct investment include:

- Drawing foreign exchange from an AD bank in India

- Capitalizing exports

- Swapping shares

- Utilizing proceeds from External Commercial Borrowings (ECBs) or Foreign Currency Convertible Bonds (FCCBs)

- Exchanging ADRs/GDRs issued by the relevant schemes and guidelines

- Using balances held in the EEFC account of the Indian Party

- Proceeds from foreign currency funds raised through ADR/GDR issues.

The obligation of Indian parties (IP) and resident individuals (RI) after making an overseas direct investment:

- Receive share certificates or other evidence of investment within six months (or a period permitted by the Reserve Bank) from the date of remittance, capitalization, or permission for capitalization.

- Repatriate all dues from the foreign entity, such as dividends, royalties, and technical fees, within 60 days of falling due (or a period permitted by the Reserve Bank).

- Submit an Annual Performance Report (APR) in Part II of Form ODI for each JV/WOS outside India by December 31 every year, based on the audited accounts from the preceding year, along with any other prescribed reports or documents.

Additional points to note:

a. The designated AD bank must monitor the receipt of documents and ensure their authenticity.

b. Certification of APRs by a Statutory Auditor or Chartered Accountant is not required for resident individuals; self-certification is acceptable.

c. If multiple IPs/RIs have invested in the same overseas JV/WOS, the one with the maximum stake is responsible for submitting the APR. Alternatively, stakeholders can mutually agree to assign this responsibility to a designated entity.

d. Reporting requirements, including submission of APR, also apply to investors in unincorporated entities in the oil sector.

e. If the host country’s law does not mandate auditing of JV/WOS books, the APR may be submitted based on un-audited accounts if certain conditions are met (e.g., certification by the Indian Party’s Statutory Auditors, adoption and ratification of accounts by the Indian Party’s Board, and not being located in a country under FATF observation or requiring enhanced due diligence).

f. All Indian businesses that have received or made Foreign Direct Investment (FDI) in the past two years must submit an annual report on foreign liabilities and assets (FLA) to the Reserve Bank of India. Every year, the FLA return has to be emailed by July 15.

Overseas Direct Investment (ODI) by Approval Route:

- Prior approval from the Reserve Bank of India (RBI) is required for all cases of direct investment or financial commitment abroad that do not fall under the automatic route. To seek approval, applicants must submit Form ODI along with necessary documents through their Authorized Dealer Category – I bank.

- When evaluating such applications, the Reserve Bank takes into account a number of factors, such as:

• The overseas JV/WOS’s viability;

• The contribution to international trade and benefits to India;

• The financial situation and business history of the Indian Party and the foreign entity;

• The Indian Party’s expertise and experience in the same or a closely related field as the JV/WOS.

3. Investments in energy and natural resources sectors exceeding the prescribed limit of financial commitment will be considered by the RBI. Applications must be forwarded by the AD Category-I – I bank as per the established procedure.

4. Proprietorship concerns, unregistered partnership firms, registered trusts, and societies engaged in manufacturing, education, or hospital sectors may make investments in a JV/WOS outside India with prior approval from the RBI. They must meet specific eligibility criteria and submit an application in Form ODI through the AD Category-I – I bank.

- Proprietorship concerns and unregistered partnership firms must be classified as ‘Status Holders’ as per the Foreign Trade Policy, have a proven track record, and comply with KYC requirements.

- Registered trusts should be established under the Indian Trust Act, of 1882, and have their trust deed permitting the proposed investment.

- Societies must be registered under the Societies Registration Act, of 1860, and have their Memorandum of Association and rules allowing the proposed investment.

5. Through an AD Category-I bank, applications should be forwarded to the Chief General Manager of the Reserve Bank of India’s Foreign Exchange Department and Overseas Investment Division. Before sending the application, together with their feedback and ideas, for consideration, the bank must make certain that the terms and criteria are met.

FAQs:

Q.) What documents are required by banks for making ODI?

- Form FC as prescribed by RBI

- Form A2 for trade outward remittance as prescribed by RBI

- Net worth certificate issued by Chartered Accountant

- Application for making ODI on the letterhead of the applicant (Format provided by the bank)

- Board Resolution authorizing proposed overseas direct investment

- Valuation certificate of the overseas party working by an Indian Chartered accountant or A-class investment banker

- The latest Audited balance sheet of the Indian Entity

- Memorandum of Association of Indian Entity (Partnership deed in case of partnership firm) and that of overseas Company confirming the object of establishment

- PAN of the Indian entity

- Share sale/purchase agreement (SPA)

Q.) Can proprietorship firms and unregistered partnership firms make ODI under an automatic route?

No, proprietorship and unregistered partnership firms cannot make ODI under automatic route but Proprietorship concerns, unregistered partnership firms, registered trusts, and societies engaged in manufacturing, education, or hospital sectors may make investments in a JV/WOS outside India with prior approval from the RBI.

Q.) What is the difference between a joint venture and a wholly owned subsidiary in the context of ODI?

“Joint Venture (JV)” signifies a foreign body constituted, documented, or incorporated in compliance with the legislation and rules of the host nation wherein the Indian Party invests directly. Whereas “Wholly Owned Subsidiary (WOS)” represents a foreign entity created, registered, or incorporated following the laws and regulations of the host nation, with the Indian Party owning its full capital. So the main difference between the both is that in a Joint venture Indian party do not own 100% shares but in WOS Indian party owns 100% share.

Q.) What does Net Worth Include with context to Overseas Direct Investment (ODI)?

For companies, net worth consists of paid-up capital and free reserves and for partnership firms, it includes Partner’s capital.

Q.) What is the maximum permitted amount for making ODI under the automatic route?

The maximum permitted amount for Overseas Direct Investment (ODI) under the automatic route is up to 400% of the net worth of the Indian entity subject to the maximum amount of USD 1 billion.

Q.) Can we invest in installments for ODI?

No, for ODI investment should be made in a single shot but if it is written in the share sale/purchase agreement that the investment can be made in two or three tranches, then it can be made in installments provided that all installments are made within 180 days of making the first installment.

Q.) What is the time limit for submission of proof/share certificate after making an ODI?

Indian investors must receive share certificates or any other valid documentary evidence of investment in the foreign entity as an eligible form of proof. The time limit for submitting this proof to the bank is within six months from the date of remittance.

Q.) What is the highest amount that a person may invest abroad?

According to the LRS’s maximum authorized limit, a resident individual may invest up to USD 250 000 in the equity shares and mandatory convertible preferred shares of a joint venture (JV) or wholly owned subsidiary (WOS) outside of India.

Q.) Is hedging permitted for overseas direct investment?

Yes, Indian entities are permitted to hedge the risk arising out of currency fluctuation through forwards and options contracts.

Q.) What are the prohibited sectors where ODI is not permitted under automatic route?

- Real estate: Investments in real estate or the purchase of immovable property, except to carry out business operations or establish a legal presence abroad.

- Banking: Investments in foreign entities that are engaged in banking or financial services, without meeting the specific regulatory requirements.

- Sectors subject to international sanctions: Investments in countries or sectors that are subject to international sanctions or embargoes, as imposed by the United Nations, the Indian government, or other relevant authorities.

- Sectors prohibited by Indian law: Investments in sectors that are explicitly prohibited by Indian law, such as gambling and betting, lottery businesses, chit funds, or Nidhi companies.

Q.) What is the time limit for submission of the Annual Performance Report (APR)?

Indian entities that have made an overseas direct investment must submit an Annual Performance Report (APR) to the RBI, through their Authorized Dealer (AD) bank. The APR provides details about the financial performance of the overseas entity and should be submitted within 6 months from the end of each financial year of the overseas entity.

Q.) Should the Indian entity repatriate the profits and dividends earned from their Overseas Direct Investment?

- Profits and dividends must be repatriated to India within a reasonable time, as per RBI guidelines. The Indian entity should not delay repatriation without valid reasons, and any delay in repatriation should be reported to the RBI through the AD bank.

- The profits and dividends can be reinvested in the overseas entity, subject to compliance with the ODI guidelines. However, the Indian entity should report such reinvestment to the RBI through their AD bank.

- Repatriation of profits and dividends should follow the laws and regulations of the host country and applicable tax treaties between India and the host country.

Overseas Direct Investment (ODI) is crucial for Indian investors seeking opportunities beyond domestic markets. The latest RBI guidelines offer valuable information on regulatory requirements and risk management strategies for venturing into international markets. With a comprehensive understanding of overseas direct investment, Indian investors can navigate the complexities of global markets and capitalize on lucrative investment prospects while mitigating potential risks. Staying abreast of ODI regulations empowers investors to make informed decisions, ensuring the success and sustainability of their ventures abroad. As the global economy continues to evolve, Indian investors can leverage ODI opportunities to diversify their portfolios and achieve long-term financial growth.

For any query and plans related to ODI, you may contact IBRLive and obtain professional consultancy.

by Neha Sharma | Dec 31, 2024 | Blog

Looking to welcome New Year 2026 with an exciting getaway without overspending? If you’re planning a budget-friendly trip, we’ve compiled a list of the world cheapest countries to travel from India. These destinations are ideal for solo travelers, couples, and families seeking adventure, culture, and relaxation without stretching their budget.

Some of these countries are cheapest country to visit from India without visa, while others are perfect for families. For smooth currency exchange before your trip, IBRLIVE India Pvt. Ltd. offers the best rates, especially for travelers from Panipat.

1. Nepal – Himalayas and Culture on a Budget

Nepal remains a favorite for Indian travelers due to visa-free access and low costs. From trekking adventures to cultural sightseeing, Nepal is ideal for a memorable New Year vacation.

Highlights:

Average Daily Cost: ₹1,500–2,500

Best For: Cheapest country to visit from India without visa

2. Vietnam – Scenic Beauty and Affordable Travel

Vietnam offers vibrant cities, stunning landscapes, and rich culture at very low costs. With cheap local foods and budget accommodations, it’s one of the world cheapest countries to travel from India.

Highlights:

Average Daily Cost: ₹2,000–3,500

3. Thailand – Family-Friendly and Budget-Conscious

Thailand continues to be a favorite for Indian travelers. Its beaches, vibrant cities, and cultural experiences are all budget-friendly. It’s perfect as a cheapest country to visit from India with family.

Highlights:

-

Temples, street food, and nightlife in Bangkok

-

Island hopping in Phuket and Krabi

-

Water sports and beach relaxation

Average Daily Cost: ₹2,500–4,000 (~1,050–1,680 THB)

Best For: Cheapest country to visit from India with family

To buy Thai currency, visit us at Panipat

4. Indonesia – Bali and More on a Budget

Indonesia, especially Bali, offers a mix of beaches, cultural experiences, and lively activities at low costs. Perfect for both solo and family travelers.

Highlights:

-

Ubud’s rice terraces and monkey forest

-

Snorkeling, surfing, and diving in Bali

-

Traditional Balinese festivals

Average Daily Cost: ₹3,000–4,500

5. Sri Lanka – Affordable Island Escape

Sri Lanka, the Pearl of the Indian Ocean, is perfect for adventure and relaxation. Indians enjoy easy visa-on-arrival, making it a cheapest country to visit from India with family.

Highlights:

-

Wildlife safaris in Yala and Udawalawe

-

Beach destinations: Bentota, Mirissa, Unawatuna

-

Cultural tours in Kandy and Galle

Average Daily Cost: ₹2,000–3,500

6. Bhutan – Mountains, Monasteries, and Magic

Bhutan is perfect for a peaceful New Year getaway. Indians enjoy visa-free travel, and the country’s landscapes, monasteries, and traditional culture are ideal for budget travelers.

Highlights:

Average Daily Cost: ₹1,800–3,000

Best For: Cheapest country to visit from India without visa

7. Cambodia – Ancient Temples at Low Cost

Home to Angkor Wat, Cambodia offers history, culture, and natural beauty at affordable rates. Budget-friendly hotels and food make it one of the world cheapest countries to travel from India.

Highlights:

Average Daily Cost: ₹1,500–3,000

8. Malaysia – Urban and Natural Wonders

Malaysia combines city life and nature while remaining affordable. Kuala Lumpur and Langkawi offer diverse experiences, making it a cheapest country to visit from India with family.

Highlights:

Average Daily Cost: ₹2,500–4,500

9. Egypt – History and Adventure on a Budget

Egypt is ideal for travelers seeking exotic experiences without high costs. Budget accommodations and cheap transport make it a unique destination.

Highlights:

Average Daily Cost: ₹3,000–5,000

10. Turkey – East Meets West Affordably

Turkey offers stunning architecture, vibrant markets, and natural beauty at affordable prices. Istanbul, Cappadocia, and Pamukkale are highlights for a memorable New Year trip.

Highlights:

-

Hot air balloon rides in Cappadocia

-

Explore Istanbul’s Grand Bazaar

-

Pamukkale’s thermal pools

Average Daily Cost: ₹3,500–6,000

FAQs – Currency Exchange Tips from IBRLIVE

1. Where is it best to exchange currency before traveling?

Use IBRLIVE India Pvt. Ltd. for competitive rates and transparent service. Panipat residents can access exclusive deals.

2. What’s the cheapest way to exchange money?

Pre-booking with IBRLIVE is usually cheaper than at airports or banks.

3. Should I exchange currency before traveling?

Yes, carrying some foreign currency beforehand avoids hidden charges abroad. IBRLIVE ensures secure and hassle-free transactions.

4. Where can I get the best exchange rates?

IBRLIVE India Pvt. Ltd. provides competitive rates and fast services, including video KYC.

Conclusion

These world cheapest countries to travel from India offer adventure, culture, and relaxation without overspending. Whether you’re traveling solo or with family, these destinations are perfect for a memorable New Year 2026 celebration. For reliable currency exchange, trust IBRLIVE India Pvt. Ltd. to get the best rates before your trip, ensuring a stress-free start to your holiday.

Best Travel Picks:

-

Cheapest country to visit from India without visa: Nepal, Bhutan

-

Cheapest country to visit from India with family: Thailand, Sri Lanka, Malaysia